Following an unprecedented election that left Americans divided and displaced, the media in battle over facts with the Trump administration, and the security of every individual uncertain and threatened, we are now witnessing an explosion of organizations and startups focused on uniting people and leveraging the power of collaboration to collect data and build technology to secure our freedom and future.

Fears of government defunding data collection, manipulating data sets and mis-communicating politically inconvenient research have inspired the founding of organizations like Data Refuge, a distributed, grassroots effort around the United States in which scientists, researchers, hackers, students, librarians and other volunteers are collecting government data to preserve it and keep it publicly accessible. Their focus on climate and environmental data is in defense of the White House removing climate data from the EPA website and screening scientific research. Others, like Open Context are helping preserve, annotate and share archeology data.

Find out what other government data is being removed from the Internet at Sunlight Foundation, where they are actively tracking the removal or changes to data sets.

Collaborative research platforms will emerge in every industry to not only aggregate and maintain integrity of data sets but also enable individuals to accelerate the development of solutions independent of government funding and policies.

This is Wikipedia on steroids and much more. Data.world is a social network exclusively for people who want to find and collaborate on building data sets. Similarly, ResearchGate provides a professional network for the scientific community to connect, collaborate, share results and drive progress. Already, more than 11 million scientists and researchers use it and are uploading more than 2.5 million publications each month.

Beyond the civic tech and education categories, this same model of empowering individuals to organize and work together to problem solve has also been successful in transportation with Waze, financial investing with Numerai, app development with GitHub, data science with Dataiku, startup solutions with ProductHunt, and many more.

Success of these platforms have initially been driven by users who are mission-driven, motivated by gamification/monetary rewards, or seeking to build an online portfolio. These platforms crossed over the chasm from passing curiosity to active and productive engagement, enabling them to truly provide more value with each user and establish a sustainable data network to help them accelerate solutions. And as these platforms grow, they will become future leaders in their industries and many will redefine our workforce.

As Washington continues to war over “Repeal and Replace” of the Affordable Care Act, one thing is certain: the need for affordable and accessible healthcare that is patient-centered and personalized. Millions of women, senior citizens, employees and independent business professionals will be affected by the expected changes to Obamacare, including, but not limited to, reduced health benefits and preventative services, discontinued subsidies, and rollback of Medicaid.

Waiting for sweeping government changes is not the solution, and development of innovative health solutions have already been underway. There’s no question that the future of healthcare is digital, where individuals are equipped to self diagnose, doctor communication is remote and timely, medication is on-demand, and data is empowering prevention, drug discovery and development. Concern and curiosity motivated me to explore our current healthcare progress and available solutions.

Remote care delivery will evolve to become the first point of contact for everything healthcare

There have been a number of telehealth startups that have entered the space in the last ten years, spanning doctor discovery and scheduling, remote care delivery, prescription management, patient monitoring and education, and more. However, remote care delivery proves to be a unique entry point with strong network effects that will enable it to quickly scale and evolve to offer services and products across the healthcare space.

While the barriers to entry are low, new entrants’ will face a difficult and costly uphill battle as they attempt to bring on high quality providers onto their platforms, and compete to secure employers and health plan contracts in advance of leaders like Teladoc, MDLive, American Well and Doctor on Demand, who are already expending significant costs to capture market share of these customers. A robust salesforce and brand awareness are key to penetration, but also not effective without offering ease of product implementation & interoperability, billing & claim filing, and regulatory compliance (HIPAA, NCQA). The strategy to secure employers and health plan contracts is an attempt to capture mass membership quickly and establish high switching costs as many self-insured employers (ASO) and insurers may only adopt one telehealth platform; according to a 2016 analysis released by the Congressional Budget Office, ~155 million Americans have employer-based health insurance coverage.

However, there is room for certain specialist-focused telehealth startups, such as Spruce, who is primarily focused on the dermatology market, which remains untapped by incumbents and accounts for >5% of annual visits, or 56 million visits. This type of specialist visit is recurring and typically costs higher (up to 3x – 4x the cost of a primary care visit).

The existing focus among players remains client growth, but the future indicator of market dominance will be member conversion and [recurring] utilization to drive PMPM, visit fees and secure client relationships. Achieving these future indicators will rely on management, business models, consumer-centered & mobile-optimized products, and seamless integration of concentric mergers.

Why now? – Political

This future of healthcare has been accelerated because of easing regulation on telemedicine definition, reimbursements and coverage. Already in 32 states and the District of Columbia there are parity laws that require private insurers to cover telemedicine visits the same way they cover in-person encounters, and in 49 states and District of Columbia reimbursements are now provided for video visits in Medicaid fee-for-service programs.

Additionally, more states have removed the requirement for a tele-presenter to be present during a virtual consultation. Finally, 18 states have enacted laws to join the Interstate Medical Licensure Compact, which will begin to grant crossborder licenses.

Why now? – Social

Easing regulation complements today’s consumer needs. Consumers no longer want to pay high costs for healthcare and are looking for more personalized care at a time when many of the other decisions they make on a daily basis have been empowered with technology and made more affordable, accessible and personalized (i.e. food, wealth management, online streaming, transportation, travel, shopping). Early direct-to-consumer fitness trackers and health apps invited consumers to increasingly value and invest in their health, and track their own progress and symptoms.

Telehealth will continue to gain traction especially at a time when Repeal and Replace Obamacare risks exacerbating lack of access and rising costs. Approximately 1/3 of all ambulatory care visits, or 417M, are treatable via telehealth, which would result in an annual saving of $6 billion in U.S. healthcare costs. Cost saving opportunities via telehealth are also true for other specialist services.

Big 4 Telehealth

The four largest telehealth players are Teladoc (NYSE: TDOC), MDLive, American Well, and Doctor on Demand. Despite Teadoc’s current leading market position with ~17M members, it still represents only a minority of the whole market.

Of these four, Doctor on Demand (DoD) is unique as it does not charge a “Per Member, Per Month” (PMPM) subscription fee, which typically costs $1 PMPM. Unlike the other three, DoD only charges visit fees, which they keep ~25%:

Medical Doctor:

$49 for a 15 min consultation

Psychology:

$79 for a 25 min consultation

$119 for a 50 min consultation

Lactation Consultant:

$99 for a 25 min consultation

$229 for a 45 min consultation

As telehealth platforms compete for employers, DoD offers an affordable option without the PMPM fee. While DoD’s model lacks the initial recurring revenue from PMPM fees, it is able to more easily align with the cost savings and ROI incentives of employers, drawing evidence that utilization rates are below 5% with other major players; Compared to Teladoc’s 5%< utilization rate, DoD boasts a much higher utilization rate of 25%-30%.

In other words, the cost per visit with Teladoc is significantly higher than $49 when factoring in PMPM. This strategy has had promising evidence as DoD now has about 400 employers (200% increase YoY) including Comcast and Union Bank & Trust, covers more than 45 million Americans and has secured relationships with UnitedHealth, Highmark*, Humana, and a number of Blue Cross Blue Shields.

*Highmark ended $1.5M contract last year with Teladoc to switch over to DoD and American Well. Most Teladoc contracts are only 1-year old…

Adoption goes both ways.

Slack, Dropbox, LinkedIn and many others have demonstrated that adoption goes both ways. And similarly, monetizing the B2B becomes much easier to achieve if you’re able to demonstrate success with B2C. DoD has since introduced a Per Provider Subscription Fee…(I don’t have numbers around this).

This is a defining time for healthcare – the winners have yet to take all and new entrants will need to be thoughtful about their unique entry point and resourceful with acquisition.

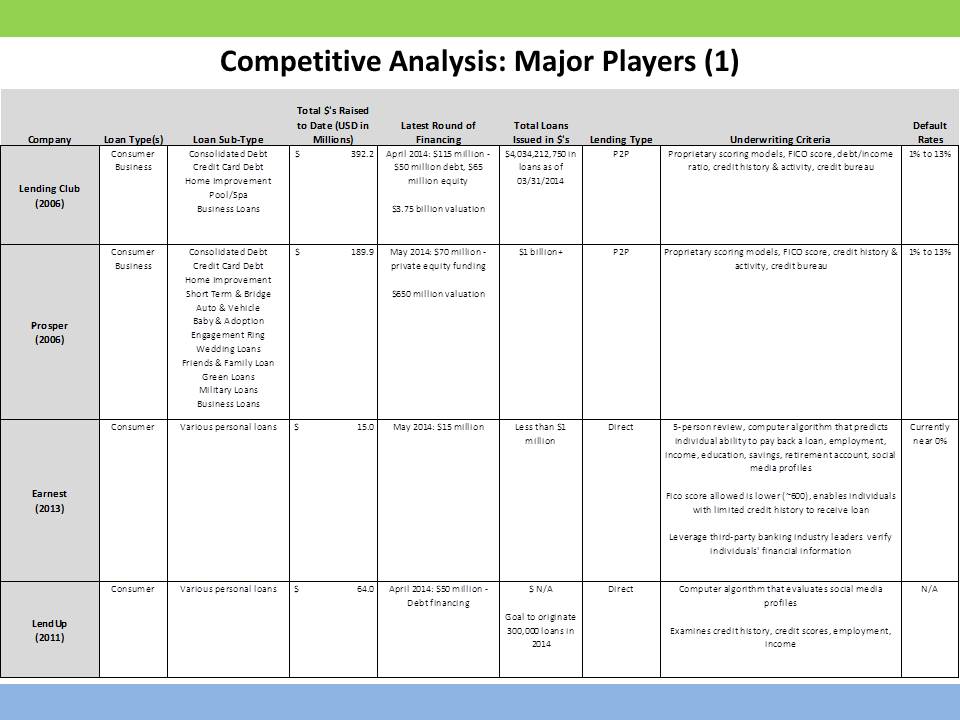

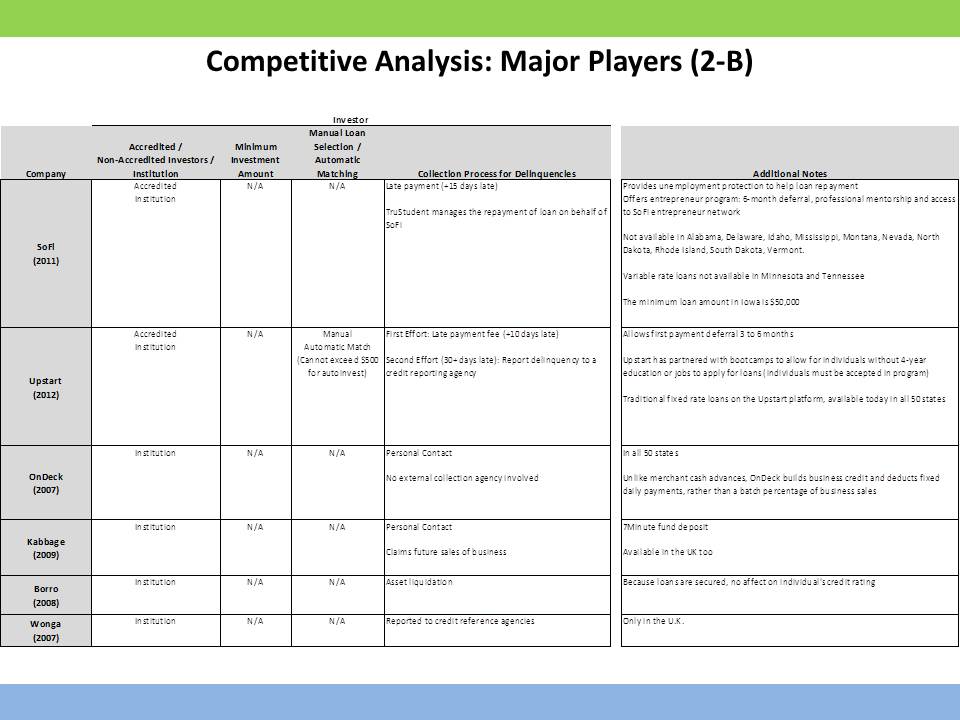

Alternative lending involves various types of loans available to consumers and business owners outside of a traditional bank loan. Alternative lending includes crowdfunding (rewards and equity-based), peer-to-peer lending (interest-based, asset-based, consumer, small business) and other non-bank financial firms.

I’ve put together a basic DevOps Market Map. Check it out, would love suggestions/feedback!

What is DevOps?

Development + Operations

DevOps is a software development method that aims to increase communication, collaboration and integration between software developers and IT operations through automation of the change, configuration and release processes, an extension of Agile Development – releasing updates to product early and often (“perpetual beta”).

* DevOps requires not only the appropriate tools but also a change in organization and culture.

The term “bubble” has been constantly and loosely used to describe the current tech industry. Most commonly, it has been used to describe any short-term price actions. But what does it really mean when we say there is a bubble? Can we even identify a bubble as it occurs? What caused its initial formation? And what catalyst will be the needle to “pop” it? Or will it ever pop and if so, is it always a bad thing? These questions are recurring with each bubble that’s formed throughout history and mostly answered in retrospect. Coming out of the most recent real estate bubble and financial crisis, individuals are overly cautious of bubble signs and are quick to conclude that a bubble exists. As such, volatility is high and valuations become unstable, but these may not indicate a “bubble” exists.

In the current environment, we observe high valuations for startups surrounded by an uncertainty about not just their profitability but also their top-line growth, new valuation metrics to evaluate fundamental value, investors that include institutions and the public, looser monetary regulations regarding funding, ease of access to capital and large follow-on investments. Wow, with that said it sounds like I should just end this post and conclude BUBBLE!! But….Back up. First, what is a bubble before we decide we are in one, and are we in danger if we are in one?

Spoiler: My definition of a bubble supports my belief that bubbles cannot be labeled in the present.

I define a bubble as a speculative process, in which high valuations of an asset or market continue to be undeserved in the long run by evaluation of its business performance, independent of economic factors. As such, in a bubble the overvaluation is purely attributed to individuals and institutions collectively driving up asset values with their expectations of achieving a profit from future price increases and the long-term growth potential of the asset, without fully understanding the invested asset and despite concerns about increasingly significant deviation from the intrinsic value of the asset.

Snapchat’s $3.2 billion valuation and $50 million investment by hedge fund Coatue Management in its Series C, BlackRock’s recent $10 billion investment in Dropbox, and increasing equity crowdfunding platforms, suggest that we are indeed experiencing inflated valuations from an influx of capital into the industry. I believe at the heart of this phenomenon is a financing effect, in which low interest rates, modern yield pigs and a depressed fixed income market are boosting institutional funds and encouraging riskier investments. Individual appetites are also riskier as a result. Additionally, with revisions to the JOBS Act, such that startups are now able to advertise their fundraising process and sell equity to qualified investors from the general public, early-stage investing is becoming more public, allowing more investors to take on a higher level of risk with investments in startups. But to conclude this financing effect has led to a bubble creation, we will need to understand investment rationales. Unfortunately, that’s not possible to do for an entire industry; however, we can gain some insight on the rationale by evaluating the businesses themselves.

Everybody’s favorite example: Snapchat

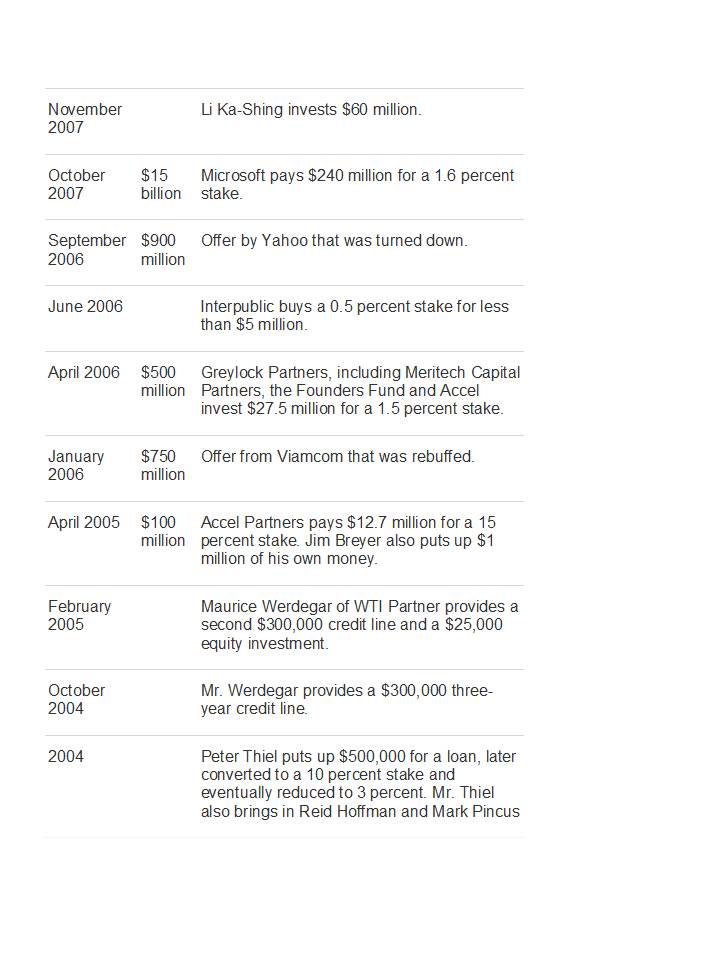

Snapchat had no revenue and was only 2-years old when it was valued at approximately $3 billion. Investors attribute the high valuation to its large user base of ~4.6 million and app usage, building in expectations that Snapchat will be able to monetize on this user base. Sounds familiar? Ah yes, what I like to call the “Facebook mentality”. But unlike Snapchat, Facebook was already generating revenue in its first year (2004). According to its S-1, Facebook made $382,000 in 2004, $9 million in 2005, $48 million in 2006 and $153 million in 2007, with no net loss. Based on the table below, 2-years old Facebook was valued at approximately $900 million, based on an offer by Yahoo that was turned down. With Snapchat, it appears that despite uncertainty of its revenue generating abilities and a recent hack that exposed the personal contact information of its users, the company along with many others is optimistic of a higher valuation than that of its $3 billion bid from Facebook. Although this example strongly supports the argument that a bubble is forming in the young tech space, according to our definition, this is not yet a bubble until we can conclude that Snapchat is unable to generate the expected revenue to support its valuation, and speculation was the main driver of value, not the business or market environment, and that many other companies in the industry are achieving valuations in this way. So you’re still not allowed to say bubble yet!

Looking at other players in the tech industry, we see that Snapchat and similar companies are more like outliers rather than lead indicators of the space.

Last year, there were a number of acquisitions and IPO’s in the 3D printing space that excited valuations and brought the technology mainstream. ExOne went public in February, closing at $26.52 a share compared to its opening price at $18. Stratasys acquired MakerBot for $403 million. Voxeljet went public with its stock priced at $13 but closed at $28.83. These days, it’s almost impossible to not hear people discuss the potential of 3D printing (especially if you’re friends with me!). But with such fast growth and share prices of listed companies skyrocketing, investors immediately assumed a bubble was in the making and fled, sending prices plummeting and bringing down valuations. Such was the case last week with 3D Systems Corp slashing its profit estimate in fear of bubble signs, sending its shares down as much as 28 percent as well as other 3D printer makers. Although these trends may follow certain theories such as Jean-Paul Rodrigue’s, in which a take-off is followed by a first sell-off from investor uncertainty about continued growth, these price volatilities do not serve as indicators for a bubble, rather they reveal cautious investors.

Looking back at the beginning of the .com bubble, the internet was a revolution with unclear boundaries for its growth and money flooded the idea from all angles. Focus quickly became on returns from quick exit strategies rather than the sustainability of the business. And there was great uncertainty about the profitability of many of the companies and the market capacity. However, when we look at the 3D printing industry, we see that there are clear paths for its growth and ability to achieve profitability. The technology’s adoption spreads across almost all industries, from aerospace to biotechnology to fashion, and has already shown signs of profitability. I believe 3D printing will significantly alter manufacturing, enhance business processes and create new business opportunities. These fundamental drivers will allow for the sustainability of 3D printing.

The aggressive funding into the industry should not be confused as excessive investment. I believe capital injection into 3D printing is helping companies in the space invest more into the technology to allow it to scale, achieve profitability and grow the market; 3D printing is a capital-intensive industry. Finally, compared to the first quarter of 2000 when ~159 internet IPOs were completed, there were only 4 publicly listed 3D printing companies at the end of 2013, with 2 IPOs occurring in 2013. I believe the limited number of public 3D printing companies is also a driver for price increase as individuals seek opportunities to invest in 3D printing but are limited to the 4. I believe the current high valuations will be justified by subsequent performance of the industry in the next few years and extreme price volatility is a short-term phenomenon as the industry is still in its youth, and therefore, I do not believe a bubble is forming in the 3D printing industry.

Evaluating the larger tech industry, I break it down into 2 parts. The first part consists of the Snapchats of the world and the second consists of companies that have proven revenue-generating businesses (i.e. Dropbox, One Kings Lane, Etsy, Twitter, Amazon) but may be currently overvalued because of their growth potential in an identified new market. The first are what I believe are “fads” and naturally the result of an ever-changing technology industry that is fueled by curiosity, innovation and excitement; they do not provide a lasting utility. Many of these “fads” will disappear after a first sell-off or a change in the economic environment (i.e. interest rates rise). The second part comprises of companies that have the potential to disrupt the current landscape and introduce efficiency or utility to individuals.

And now, to finally get to the point, I don’t think we are necessarily in a tech bubble, but are seeing a lot of attention around some fads; however, we need to be cautious and observe what is being funded, understand why it is being funded and question if funding would have occurred given a different economic environment.

You must be logged in to post a comment.