The term “bubble” has been constantly and loosely used to describe the current tech industry. Most commonly, it has been used to describe any short-term price actions. But what does it really mean when we say there is a bubble? Can we even identify a bubble as it occurs? What caused its initial formation? And what catalyst will be the needle to “pop” it? Or will it ever pop and if so, is it always a bad thing? These questions are recurring with each bubble that’s formed throughout history and mostly answered in retrospect. Coming out of the most recent real estate bubble and financial crisis, individuals are overly cautious of bubble signs and are quick to conclude that a bubble exists. As such, volatility is high and valuations become unstable, but these may not indicate a “bubble” exists.

In the current environment, we observe high valuations for startups surrounded by an uncertainty about not just their profitability but also their top-line growth, new valuation metrics to evaluate fundamental value, investors that include institutions and the public, looser monetary regulations regarding funding, ease of access to capital and large follow-on investments. Wow, with that said it sounds like I should just end this post and conclude BUBBLE!! But….Back up. First, what is a bubble before we decide we are in one, and are we in danger if we are in one?

Spoiler: My definition of a bubble supports my belief that bubbles cannot be labeled in the present.

I define a bubble as a speculative process, in which high valuations of an asset or market continue to be undeserved in the long run by evaluation of its business performance, independent of economic factors. As such, in a bubble the overvaluation is purely attributed to individuals and institutions collectively driving up asset values with their expectations of achieving a profit from future price increases and the long-term growth potential of the asset, without fully understanding the invested asset and despite concerns about increasingly significant deviation from the intrinsic value of the asset.

Snapchat’s $3.2 billion valuation and $50 million investment by hedge fund Coatue Management in its Series C, BlackRock’s recent $10 billion investment in Dropbox, and increasing equity crowdfunding platforms, suggest that we are indeed experiencing inflated valuations from an influx of capital into the industry. I believe at the heart of this phenomenon is a financing effect, in which low interest rates, modern yield pigs and a depressed fixed income market are boosting institutional funds and encouraging riskier investments. Individual appetites are also riskier as a result. Additionally, with revisions to the JOBS Act, such that startups are now able to advertise their fundraising process and sell equity to qualified investors from the general public, early-stage investing is becoming more public, allowing more investors to take on a higher level of risk with investments in startups. But to conclude this financing effect has led to a bubble creation, we will need to understand investment rationales. Unfortunately, that’s not possible to do for an entire industry; however, we can gain some insight on the rationale by evaluating the businesses themselves.

Everybody’s favorite example: Snapchat

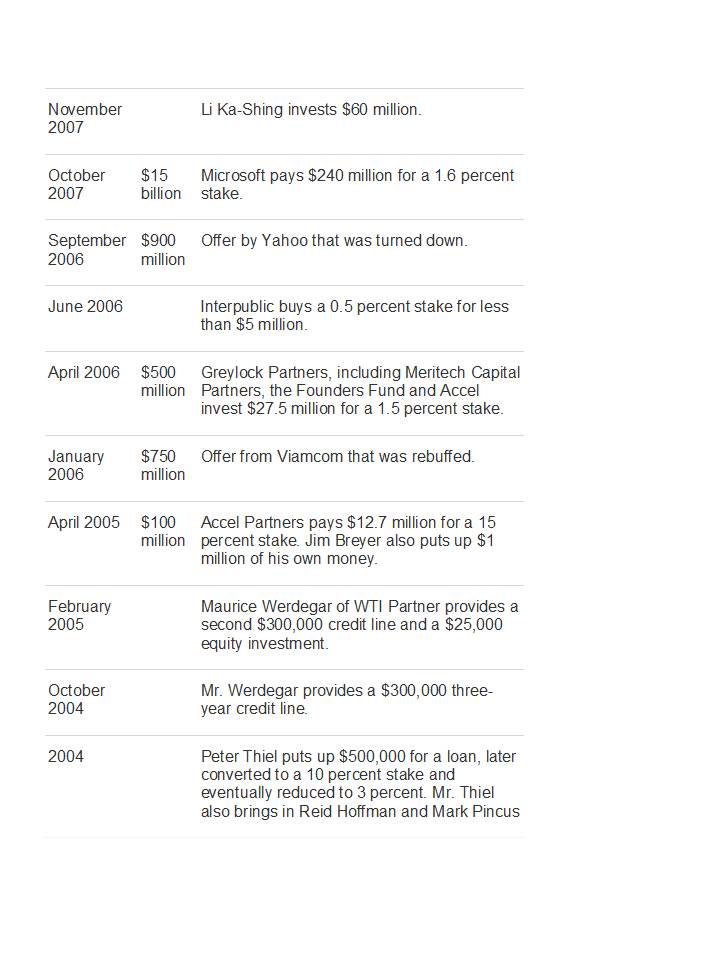

Snapchat had no revenue and was only 2-years old when it was valued at approximately $3 billion. Investors attribute the high valuation to its large user base of ~4.6 million and app usage, building in expectations that Snapchat will be able to monetize on this user base. Sounds familiar? Ah yes, what I like to call the “Facebook mentality”. But unlike Snapchat, Facebook was already generating revenue in its first year (2004). According to its S-1, Facebook made $382,000 in 2004, $9 million in 2005, $48 million in 2006 and $153 million in 2007, with no net loss. Based on the table below, 2-years old Facebook was valued at approximately $900 million, based on an offer by Yahoo that was turned down. With Snapchat, it appears that despite uncertainty of its revenue generating abilities and a recent hack that exposed the personal contact information of its users, the company along with many others is optimistic of a higher valuation than that of its $3 billion bid from Facebook. Although this example strongly supports the argument that a bubble is forming in the young tech space, according to our definition, this is not yet a bubble until we can conclude that Snapchat is unable to generate the expected revenue to support its valuation, and speculation was the main driver of value, not the business or market environment, and that many other companies in the industry are achieving valuations in this way. So you’re still not allowed to say bubble yet!

Looking at other players in the tech industry, we see that Snapchat and similar companies are more like outliers rather than lead indicators of the space.

Another favorite example: 3D Printing

Last year, there were a number of acquisitions and IPO’s in the 3D printing space that excited valuations and brought the technology mainstream. ExOne went public in February, closing at $26.52 a share compared to its opening price at $18. Stratasys acquired MakerBot for $403 million. Voxeljet went public with its stock priced at $13 but closed at $28.83. These days, it’s almost impossible to not hear people discuss the potential of 3D printing (especially if you’re friends with me!). But with such fast growth and share prices of listed companies skyrocketing, investors immediately assumed a bubble was in the making and fled, sending prices plummeting and bringing down valuations. Such was the case last week with 3D Systems Corp slashing its profit estimate in fear of bubble signs, sending its shares down as much as 28 percent as well as other 3D printer makers. Although these trends may follow certain theories such as Jean-Paul Rodrigue’s, in which a take-off is followed by a first sell-off from investor uncertainty about continued growth, these price volatilities do not serve as indicators for a bubble, rather they reveal cautious investors.

Looking back at the beginning of the .com bubble, the internet was a revolution with unclear boundaries for its growth and money flooded the idea from all angles. Focus quickly became on returns from quick exit strategies rather than the sustainability of the business. And there was great uncertainty about the profitability of many of the companies and the market capacity. However, when we look at the 3D printing industry, we see that there are clear paths for its growth and ability to achieve profitability. The technology’s adoption spreads across almost all industries, from aerospace to biotechnology to fashion, and has already shown signs of profitability. I believe 3D printing will significantly alter manufacturing, enhance business processes and create new business opportunities. These fundamental drivers will allow for the sustainability of 3D printing.

The aggressive funding into the industry should not be confused as excessive investment. I believe capital injection into 3D printing is helping companies in the space invest more into the technology to allow it to scale, achieve profitability and grow the market; 3D printing is a capital-intensive industry. Finally, compared to the first quarter of 2000 when ~159 internet IPOs were completed, there were only 4 publicly listed 3D printing companies at the end of 2013, with 2 IPOs occurring in 2013. I believe the limited number of public 3D printing companies is also a driver for price increase as individuals seek opportunities to invest in 3D printing but are limited to the 4. I believe the current high valuations will be justified by subsequent performance of the industry in the next few years and extreme price volatility is a short-term phenomenon as the industry is still in its youth, and therefore, I do not believe a bubble is forming in the 3D printing industry.

Evaluating the larger tech industry, I break it down into 2 parts. The first part consists of the Snapchats of the world and the second consists of companies that have proven revenue-generating businesses (i.e. Dropbox, One Kings Lane, Etsy, Twitter, Amazon) but may be currently overvalued because of their growth potential in an identified new market. The first are what I believe are “fads” and naturally the result of an ever-changing technology industry that is fueled by curiosity, innovation and excitement; they do not provide a lasting utility. Many of these “fads” will disappear after a first sell-off or a change in the economic environment (i.e. interest rates rise). The second part comprises of companies that have the potential to disrupt the current landscape and introduce efficiency or utility to individuals.

And now, to finally get to the point, I don’t think we are necessarily in a tech bubble, but are seeing a lot of attention around some fads; however, we need to be cautious and observe what is being funded, understand why it is being funded and question if funding would have occurred given a different economic environment.

So, nope, still can’t say bubble!

But go ahead and call this a bubble…

I don’t think online education can or will replace the prestige of attendance at an established university in China or abroad, but I do believe it will complement it. I had previously thought online education would allow for individuals who could not afford to study abroad to gain access to the resources provided at those foreign universities; however, I have found that Chinese students who study abroad are not evaluated on the content studied abroad but rather their experience. Also, I have found that Chinese students are motivated to study abroad for 2 main reasons, which do not include access to foreign content: (1) It is a way to avoid the College National Exam / local university pressure and (2) younger students are able to enhance and practice their English (English is a school subject in China and is a full separate section on the College National Exam). Additionally, this past October, a group of top Chinese universities partnered to launch their own MOOC and learning portal (similar to edX launched by Harvard, MIT and Berkeley). Given these reason, I don’t think the online education opportunity is in traditional/higher education.

As China transitions from its manufacturing and export-dependent economy to a services and skills-based economy, it will require a more skilled workforce to meet those market demands, suggesting the need for increased vocational education opportunities. That vocational education has been historically perceived as a low-status education compared to academic-based education (theory over practice belief), suggests that there is a strong divide between the two and students are unable to easily gain access to both. This traditional ideology naturally encourages students to pursue an academic-based education, creating a workforce that is over-educated but under-skilled. Additionally, given the competitive job market in China right now (~16% of the record ~7 million Chinese university graduates last year were unemployed), there is increased value in additional learning/training for individuals. Finally, the need for innovation is necessary for China to maintain its growth, supply jobs and become a knowledge economy, and to fuel that innovation will require access to content beyond school borders and local resources. This may be where the online education opportunity lies.

Of course, the challenge lies in Chinese government intervention and facilitation of online education. So far, there are few foreign online education companies that have been able to successfully expand into China, with the exception of Coursera as of the end of last year, in which it partnered with an internet site to launch on that site. And local companies will struggle to compete with the government/university-backed online offerings (especially if they start to offer not only academic courses but vocational/technical trainings) as they will find it difficult to compete for online enrollment of students and brand themselves as a credible learning site. I think a company that is focused on offering courses and resources and building a community around a certain subject (become the go-to online destination to learn coding or personal finance or a language), such as Codecademy, will thrive given the current Chinese learning environment.

The end of standardization has been realized for many years now, and it is even more apparent today as companies compete to break into international markets. We are seeing this with ecommerce companies, sharing services, fashion houses, pharmaceutical companies and a host of other businesses. Achieving international market growth is not easy and involves constant development of product, brand and distribution strategy as well as awareness of the government’s role in the country and the country’s policies and plans.

By evaluating McDonald’s we can learn effective strategies on how to “think global, act local”. Over the years, McDonald’s has continued to innovate its menu and adapt its go-to market system, allowing it to maintain its leading global presence, retain its customers and uphold its reputation as the “Golden Arches”. Many companies are able to break into a new country or environment quickly but fail to tailor their products and services to the needs and demands of its local customers. Localization must be applied at every level of the business to achieve successful international market growth.

A comparison of the different McDonald’s website by country shows us the importance of brand consistency, language, design and variation of product offerings to accommodate local market conditions.

United States

China

France

Japan

Most noticeable is the use of color to develop brand recognition and connect with local customers. The golden arches are displayed in the upper left corner of each of its websites and yellow is a commonly used color across all the sites. However, notice the McDonald’s French and German websites have replaced the iconic red background with green. This color change in 2009 was intended to aggressively communicate a more eco-friendly image to help the company connect with a pro “green” customer base in Europe. In this instance, color was a driver to reflect shared values between the business and its customers, suggesting that the original red and yellow logo colors were not well received in Europe and some separation from the U.S. home company image was necessary.

At a NYC Hacker Growth Event I attended last November, a former LinkedIn employee shared his experiences with launching LinkedIn abroad and how they came across the language factor. They found that using the local language (initially launched in English) on the website for that country led to increased engagement. Yes, this sounds obvious but many companies have failed to do this and just think how challenging it will be for young companies with blogs to accurately translate their posts across their different websites (God forbid a grammatically incorrect and Babblefish translation!).

Language is the medium of culture, allowing a group of individuals to share their knowledge, beliefs, values, attitudes, politics and religion. And because culture is largely tied to identity and influences our interactions (human-human and human-product interaction), decision-making and interests, language is key when building brand equity abroad. As my best friend Erica Baba beautifully summarized:

“If we look at culture on an individual basis, we can see the impact of one’s cultural ideologies and values on the way one lives and carries himself or herself. Everywhere we go, we bring with us our culture. You see, there are things we all choose to do or ways we choose to be because of the cultures we identify with and what they mean to us.”

Allowing an individual to visit a website in his or her own language gives the individual a sense of ownership of the site (most basic form of personalization), allows the individual to easily navigate the pages and explore features, and adds content to the products offered. As a result, the individual is more likely to return and a community is more easily formed, which is crucial for marketplaces as they expand abroad.

Beyond cross-cultural design and language, and equally as important, are localized products, services and payment options. Product adaptation and innovation enhance a company’s product offerings because it is tailored to local preferences and culture. For example, McDonald’s in India does not have beef or pork on its menu (a friend of mine found this out when trying to order a beef burger there…). And did you know that once a year in China, McDonald’s offers the Prosperity Burger in celebration of Chinese New Year? McDonald’s has also recently launched a new “rice based” menu in China this past year and The McCamembert, a burger with the French Camembert cheese, in France. The geographic variations to its menus demonstrate McDonald’s sensitivity and adaptability to local cultures and preferences.

Check out a few more menu options outside the U.S. here.

Product inventions aren’t always successes (Some of the stuff Taco Bell has introduced is total crap!) but more often than not they resonate with the local consumer. Product variations should also account for demographics, infrastructure and local trends (e.g. the international car market is particularly sensitive to age group, lifestyle and roads when designing and selling cars to a region).

In addition to menu innovation, McDonald’s has also continued to reinvent its space. The McCafe was introduced in Europe to adopt the European café lifestyle, capitalize on the growing coffee trend at the time and offer customers a new breakfast option. And just this past November, Starbucks introduced a new store concept in its Beijing store that was inspired by China’s one-child policy atmosphere and aimed to create a hub for the number of young people near the location.

From the product and service to the product packaging to the company website, the brand is continuously being built and communicated. The consumers’ knowledge, impression and experience with the product or service will determine the viability and sustainability of the business.

Localized payment methods can best be examined with Flipkart, India’s first billion-dollar internet startup, and Amazon. Both Flipkart and Amazon offer Cash on Delivery (COD)—the individual pays for the good upon delivery in cash. According to an article from May 2013, there are less than 20 million credit cards in circulation in India, representing a penetration rate of about 1.7% among the country’s 1.2 billion population. Additionally, approximately 70% of Flipkart’s transactions are currently completed using COD. This phenomenon is largely tied to Indian culture, which maintains a leery attitude towards non-cash transactions because of its intangible nature (the physical exchange of cash or gold is symbolic in Indian culture) and perceived lack of security and transparency. I believe the following excerpt from a research paper titled “Facilitating Global E-Commerce: A Comparison of Consumers’ Willingness to Disclose Personal Information Online in the U.S. and in India” also helps explain some of the resistance to credit adoption:

“In India, because of its collectivistic culture, consumers may be more willing to extend and preserve their relationship with an organization because it is seen as part of an extended community… Consequently, their desire to maintain the relationship is realized through sharing of personal information.”

Flipkart achieved fast adoption and significant growth in India because it offered services and payment methods that revolved around India’s transaction preferences. In one year, the company increased its customer base by more than ten times from 0.2 million to 2.08 million as well as increased its website visits from 40 million to 102 million. Amazon was quick to observe this and prepared to tap the attractive Indian ecommerce market, and since launching Amazon.in, it is also offering COD (although COD is currently only available for Amazon fulfilled products). Despite COD being the more expensive payment method for the company, Amazon is offering this payment option because it realizes user acquisition would not be possible without adapting to local methods of transaction in India.

Finally, awareness of the local government and legal regulations is extremely necessary as a company looks to expand beyond its domestic borders. There is significant operating risk from a government that is unsupportive of foreign businesses and that highly regulates marketing activities and distribution channels. Such is the case in India and China, in which the government becomes a priority customer to the firm.

Of course, this is easier said than done and it will take time. Localization will require not only an immense amount of research and capital at entry, but also throughout the existence of the business abroad as trends, values, beliefs, attitudes, politics, etc. in a country are ever-evolving. Remember, quick growth is not always good growth.

I was hesitant to write this post as I realize I’m about to share more from my heart than from my head. Only my very first post was a personal post…But I think my readers deserve to get to know me a little better.

2013 was my first full year outside of California. It wasn’t easy being so far away from friends and family, and I found myself searching for any excuse to visit home (frequent flight deals made it too easy!). But don’t get me wrong, I Love New York and don’t have any regrets about the day I said yes to the job that would fly me to the other coast. I’ve learned to not only adapt but also embrace the density of the city, the constant energy in the streets, the intimidating tall buildings, the always-crowded restaurants and lounges, the rush on the subways, and even the snow (but more so because the humid summers are so much worse..). I also love that the east coast brings me so much closer to Europe, where most of my 2014 travels will be planned! And I have to share that I am now able to walk numerous blocks in high heels (my Rainbows have been a little idle).

It’s been a tough but very fun year trying to balance my full-time job as a valuation analyst with my new blog and increased involvement in the NY tech community. I love the challenge. It fuels me and makes me feel alive.

If you’ve been following my recent tweets, you will notice a number of mentions about 3D Hubs, a collaborative platform for 3D printer owners and 3D makers (Check them out!). I’ve been assisting the 3D Hubs US team in their efforts to build out their US presence and some of you may have seen my blog post for their new Designer Series on Francis Bitonti (more to comeJ!). Looking back, I feel very fortunate to have come across these opportunities. But I am even more grateful for the friends I’ve made along the way this past year. Each new friend opened my mind and eyes a little more, taught me something new, helped me find my passion and gave me the confidence to take risks as I pursue my passions. To my new friends, if you’re reading this, thank you.

Looking forward, I hope to foster both the old and new relationships and grow with them. Relationships are hard to maintain in our busy schedules, and I would argue that friendship can sometimes be more easily lost than gained without constant effort, especially as we get older because new priorities emerge. As such, my first new year’s resolution is to always be connecting (My A-B-C) with family, friends and even acquaintances. This also encompasses connecting with new individuals as well. I believe often times the most powerful conversations we have are with strangers because the new stories and information exchanged help us discover something about ourselves and the world in that very moment.

My second resolution is to take more risks. Looking back on 2013, I’ve realized I am more risk averse than I believed myself to be. Today, twenty-somethings are more focused on getting ahead in their careers early on and establishing a stable income after a few years of work. Financial instability is not as acceptable as it was in previous generations as education and resources are more readily available for our generation (we have the benefit of both online and offline learning tools), preparing us better to attain a job opportunity. But we have to recognize the world is taking more risks on our generation and our ideas. The most recent investments in what may have initially appeared as a crazy idea (well, I still think Snapchat is crazy…) was a door to endless opportunities for development in science, health, finance, education, human interaction and so much more. Not sure where my first risky step will be, but I promise you it will be towards something I am passionate about and that I believe will change and improve people’s lives, and not driven by financial incentives.

My third resolution is to continue to be forever young. There are some things you can only do when you’re young and I plan to not miss out. I travelled a lot in 2013 and I intend to do that again! Travel is a beautiful experience to me. It is the perfect combination of isolation and constant interaction, a discovery process both within and around us. I also challenge myself to be more spontaneous, something I believe is a behavior of the youth and will keep us on our toes. Sometimes, too much thinking holds us back from a great opportunity! As one professor in college once advised me, “Just do it, Tiffany! Head down and go for it!” One of the best advices I’ve ever gotten.

And some final thoughts and goals…

A year from today, I hope to continue to share interesting blog posts with my family, friends and readers. I admire individuals who have been blogging for many years. Consistent posts aren’t easy and I found that out after only 4 months!

A year from today, I hope to be doing more of what I love.

A year from today, I wish to still not have any regrets because I never didn’t “Just Do It”.

Happy New Year, Friends!

12/31/2013

You must be logged in to post a comment.